What Is a Portfolio Acquisition Approach?

What Is a Portfolio Acquisition Approach?

A portfolio acquisition approach is defined as the deliberate purchase of multiple related businesses or assets together to create enterprise value greater than each individual acquisition would generate alone. This strategy, commonly called “buy-and-build” in private equity and M&A circles, relies on two core mechanics: multiple arbitrage and integration synergies. Multiple arbitrage works by acquiring smaller companies at 4–5x EBITDA and combining them into a platform that commands 7–10x EBITDA valuations, significantly increasing overall enterprise value. For business owners and entrepreneurs, understanding what is a portfolio acquisition approach means recognizing it as a growth engine, not just a transaction.

What is a portfolio acquisition approach, and how does it work?

A portfolio acquisition strategy groups targeted companies under one ownership structure to unlock scale, market share, and pricing power that no single business could achieve independently. The approach is methodical. You identify a platform company first, then layer in complementary acquisitions over time.

The buy-and-build model is the most recognized framework. A platform company serves as the foundation. Add-on acquisitions then expand its capabilities, geography, or customer base. The result is a combined entity that earns a higher valuation multiple than any individual component.

Three forces drive the value creation:

- Scale advantages: Combined revenue and cost structures reduce per-unit overhead.

- Market positioning: A larger entity commands stronger negotiating power with suppliers and customers.

- Multiple arbitrage: The valuation gap between small and large companies is the financial engine of the entire strategy.

What are the main types of portfolio acquisition strategies?

Portfolio acquisition methods fall into four distinct categories. Each serves a different strategic purpose, and choosing the wrong type for your goals wastes capital and management attention.

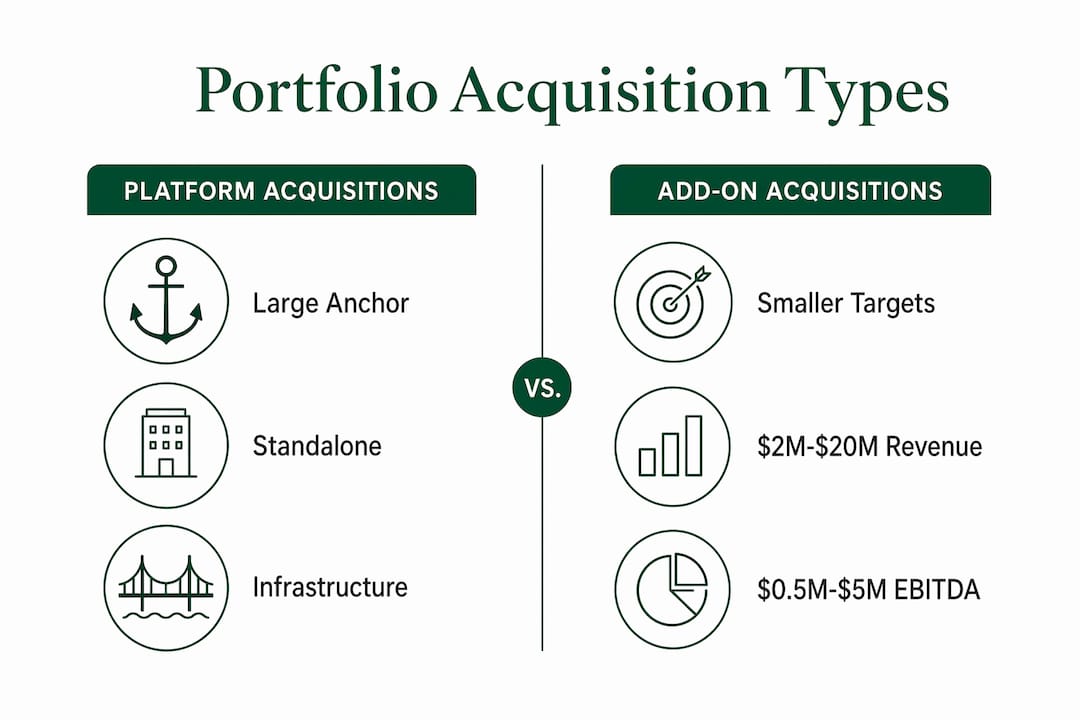

Platform vs. add-on acquisitions

A platform acquisition is the anchor. It is typically a larger, well-managed business with existing infrastructure, management depth, and a defensible market position. Everything else builds on top of it.

An add-on acquisition targets smaller companies, typically in the $2M–$20M revenue range with $0.5M–$5M EBITDA, that complement the platform. Sizing matters here. A target too small adds integration costs without meaningful revenue lift. A target too large introduces merger complexity that can derail operations.

Bolt-on and tuck-in distinctions

Bolt-on acquisitions retain some operational independence after purchase. The acquired company keeps its brand, team, and processes but gains access to the platform’s resources and distribution.

Tuck-in acquisitions are fully absorbed into the platform. The acquired entity loses its separate identity. This approach maximizes cost synergies but requires stronger integration management.

| Type | Size | Integration Level | Primary Goal |

|---|---|---|---|

| Platform | Large anchor | Standalone | Foundation for growth |

| Add-On | $2M–$20M revenue | Moderate | Expand capabilities or geography |

| Bolt-On | Small to mid | Partial | Preserve brand, add resources |

| Tuck-In | Small | Full absorption | Maximize cost synergies |

How do you source and select the right acquisition targets?

Target selection is where most portfolio strategies succeed or fail. Opportunistic acquisition without defined criteria produces a fragmented portfolio that destroys value instead of building it. The discipline starts before you ever contact a seller.

Define your acquisition criteria first

Criteria should cover four dimensions: target geography, revenue size, capability gaps the acquisition fills, and cultural fit indicators. Oliver Wyman’s M&A consulting practice confirms that defining criteria upfront improves portfolio discipline and investment outcomes. Without this filter, you waste time evaluating businesses that will never fit your thesis.

Steps to source acquisition targets

- Build your criteria document. Define geography, revenue range, EBITDA floor, industry focus, and deal-breaker conditions.

- Map the market. Use industry databases, trade associations, and LinkedIn to identify companies that match your profile.

- Prioritize off-market targets. Direct outreach before brokers enter the process keeps multiples lower and reduces auction competition.

- Profile owners. Research tenure, age, succession plans, and motivations. Owners approaching retirement or facing succession gaps are often receptive to early conversations.

- Initiate contact. Send a personalized letter or email that speaks to the owner’s specific situation, not a generic acquisition inquiry.

- Screen and rank. Score each target against your criteria before committing to a formal process.

Pro Tip: Owner profiling is the most underused sourcing tactic. An owner who has run a business for 25 years and has no succession plan is a far warmer prospect than one who just hired a CFO. Build a contact list of these profiles and reach out 12–18 months before you need the deal to close.

What are best practices for integrating portfolio acquisitions?

Integration is where acquisition value is either realized or lost. Financial diligence tells you what you are buying. Integration discipline determines what you actually keep.

Cultural due diligence is non-negotiable

Culture clash is a leading cause of acquisition integration failure, according to CliftonLarsonAllen. Financial models do not capture whether two management teams will work together productively. Assess cultural alignment during diligence, not after close.

Key cultural indicators to evaluate:

- Decision-making style: Centralized vs. decentralized authority structures

- Communication norms: Formal reporting vs. open-door cultures

- Performance expectations: How each company defines and rewards results

- Employee tenure and loyalty: High tenure signals stability; high turnover signals risk

Build a 100-day integration strike team

A dedicated cross-functional team assigned to manage the first 100 days post-close significantly improves acquisition success rates. This team owns org alignment, systems integration, and KPI tracking. It is not a committee. It has authority, a clear mandate, and a defined timeline.

Track KPIs that connect directly to your deal thesis. If the thesis was revenue synergies from cross-selling, measure pipeline growth and new customer acquisition from the combined entity within 90 days. If the thesis was cost reduction, track headcount and vendor consolidation weekly.

Experts at CliftonLarsonAllen also advocate a one-page vision map that defines the combined company’s mission and goals. This document aligns internal teams on why the acquisition happened and where the business is heading.

Pro Tip: Celebrate early integration wins publicly. When two teams see that the combined entity hit its first shared revenue milestone, skepticism drops and collaboration accelerates. Small wins in the first 30 days build the trust that sustains the harder work in months two and three.

What tax and financial factors affect portfolio acquisitions?

Tax structure is one of the most consequential decisions in any portfolio acquisition. Getting it wrong on a large deal can cost hundreds of thousands of dollars in avoidable liability.

Linked transaction rules and stamp duty

In property-heavy portfolio acquisitions, linked transaction rules under s108 FA2003 aggregate multiple purchases for tax purposes. Following the 2024 abolition of Multi-Dwelling Relief, each property is taxed on its individual consideration. The aggregation effect of marginal rates and the 5% additional property surcharge means that on a £5,000,000 portfolio, the Stamp Duty Land Tax bill can exceed £400,000. That figure represents a material deal cost that must appear in your financial model before you sign a letter of intent.

Share purchase vs. direct asset acquisition

The structure of the deal changes the tax outcome significantly. A share purchase attracts 0.5% stamp duty compared to higher rates on direct asset acquisitions. The trade-off is real. Share purchases inherit the target company’s existing liabilities, including undisclosed tax obligations, pending litigation, and legacy contracts. Direct asset acquisitions cost more in transfer taxes but give the buyer a clean liability profile.

| Structure | Stamp Duty Rate | Liability Exposure | Best Use Case |

|---|---|---|---|

| Share Purchase | 0.5% | Inherits all corporate liabilities | Clean targets with strong diligence |

| Direct Asset Acquisition | Higher (varies by asset class) | Buyer selects assets and liabilities | Asset-heavy or complex liability situations |

| Property Portfolio (post-2024) | Marginal rates + 5% surcharge | Linked transaction aggregation applies | Requires specialist tax counsel |

Engage specialist tax counsel before structuring any portfolio deal. Tax modeling at the letter-of-intent stage, not at closing, protects your returns.

Key takeaways

A portfolio acquisition approach creates enterprise value by combining multiple targeted businesses under one ownership structure, using multiple arbitrage, disciplined integration, and tax-efficient deal structuring to maximize returns.

| Point | Details |

|---|---|

| Define criteria before sourcing | Set geography, revenue size, and capability gaps before contacting any target. |

| Off-market outreach wins | Direct contact before broker involvement keeps multiples lower and fit higher. |

| Integration requires a dedicated team | A 100-day cross-functional strike team improves post-close success rates measurably. |

| Cultural fit is a financial variable | Culture clash drives talent loss and customer churn, directly reducing deal returns. |

| Tax structure shapes deal economics | Share purchases and direct asset acquisitions carry different stamp duty and liability profiles. |

Why execution discipline separates portfolio winners from losers

Most business owners I work with understand the concept of portfolio acquisition quickly. The definition is not the hard part. The execution is where deals unravel, and the patterns are consistent enough to be predictable.

The first mistake is treating acquisition criteria as flexible. When a deal looks attractive on price but does not fit your defined geography or capability profile, the temptation to rationalize is strong. Resist it. Every exception to your criteria introduces a business that will demand disproportionate management attention and produce below-thesis returns.

The second mistake is underestimating integration timelines. Entrepreneurs who have built businesses organically often assume that two well-run companies will naturally combine well. They do not. Systems, incentive structures, and reporting cultures need active alignment. The 100-day integration framework from CliftonLarsonAllen exists precisely because passive integration fails.

The emerging opportunity I see most clearly is in lower-middle-market services businesses, particularly those in fragmented industries where no dominant regional player exists yet. Healthcare services, specialty trades, and professional services firms are all sectors where a disciplined buy-and-build approach can create a market leader within three to five years. The businesses are available, the owners are often motivated, and the multiple arbitrage is real. The constraint is always execution quality, not deal flow.

If you are considering a portfolio strategy, start with one platform acquisition and one add-on before scaling. Prove your integration model works before you replicate it six times.

— Sierra

How Compassbusinessacquisitions supports your portfolio strategy

Building a portfolio of businesses requires more than capital. It requires verified deal flow, accurate valuations, and a network of motivated sellers who are ready to transact.

Compassbusinessacquisitions specializes in connecting buyers with businesses that match their acquisition criteria, whether you are sourcing a platform company or adding a bolt-on to an existing portfolio. Their professional valuation process gives you a credible financial foundation for every deal, and their targeted marketing reaches sellers who are genuinely ready to move. For entrepreneurs ready to act, explore businesses for sale through Compassbusinessacquisitions and find opportunities aligned with your growth thesis. You can also connect directly with their expert broker team to discuss your specific acquisition criteria and get matched with qualified targets.

FAQ

What is the definition of portfolio acquisition?

A portfolio acquisition is the purchase of multiple businesses or assets together under one ownership structure to create combined value greater than each individual acquisition. The strategy typically uses buy-and-build mechanics and multiple arbitrage to increase enterprise value.

How does multiple arbitrage work in a portfolio acquisition strategy?

Multiple arbitrage works by acquiring smaller companies at lower valuation multiples, typically 4–5x EBITDA, and combining them into a platform that commands higher multiples of 7–10x EBITDA. The gap between acquisition price and exit valuation is the primary source of financial return.

What is the difference between a bolt-on and a tuck-in acquisition?

A bolt-on acquisition retains the acquired company’s brand and operational identity while connecting it to the platform’s resources. A tuck-in acquisition fully absorbs the target into the platform, eliminating its separate identity to maximize cost synergies.

How do you find off-market acquisition targets?

Direct outreach to business owners before brokers are engaged is the most effective method. Profiling owners by tenure, age, and succession readiness identifies the most receptive prospects and avoids the valuation inflation that comes with competitive auction processes.

What tax risks apply to property portfolio acquisitions?

Following the 2024 abolition of Multi-Dwelling Relief, linked transaction rules can aggregate multiple property purchases for Stamp Duty purposes, producing bills that exceed £400,000 on a £5,000,000 portfolio. Engaging specialist tax counsel before structuring the deal is the standard practice for managing this exposure.