Tuck-In Acquisition Strategy: A Leader's Growth Guide

Tuck-In Acquisition Strategy: A Leader’s Growth Guide

A tuck-in acquisition strategy is defined as the full absorption of a smaller company into an acquirer’s existing operations, causing the target to cease independent existence entirely. This approach gives business leaders a direct path to rapid scaling, niche capability gains, and cost efficiencies that organic growth rarely matches. Unlike large transformational mergers, tuck-in deals carry a lower financial risk profile and a tighter integration scope. Compassbusinessacquisitions works with buyers and sellers navigating exactly this kind of targeted deal, connecting strategic acquirers with businesses that fit their growth roadmap. Understanding how this model works, where it outperforms other acquisition types, and where it fails is the foundation of any serious growth plan.

What is a tuck-in acquisition strategy and how does it work?

A tuck-in acquisition is when a larger company fully absorbs a smaller target into its existing structure, with the acquired business losing its separate identity. The acquired company’s assets, customers, staff, and intellectual property transfer directly into the buyer’s operations. No parallel brand or subsidiary structure survives. The result is a single, consolidated business that is larger, more capable, and more competitive than before.

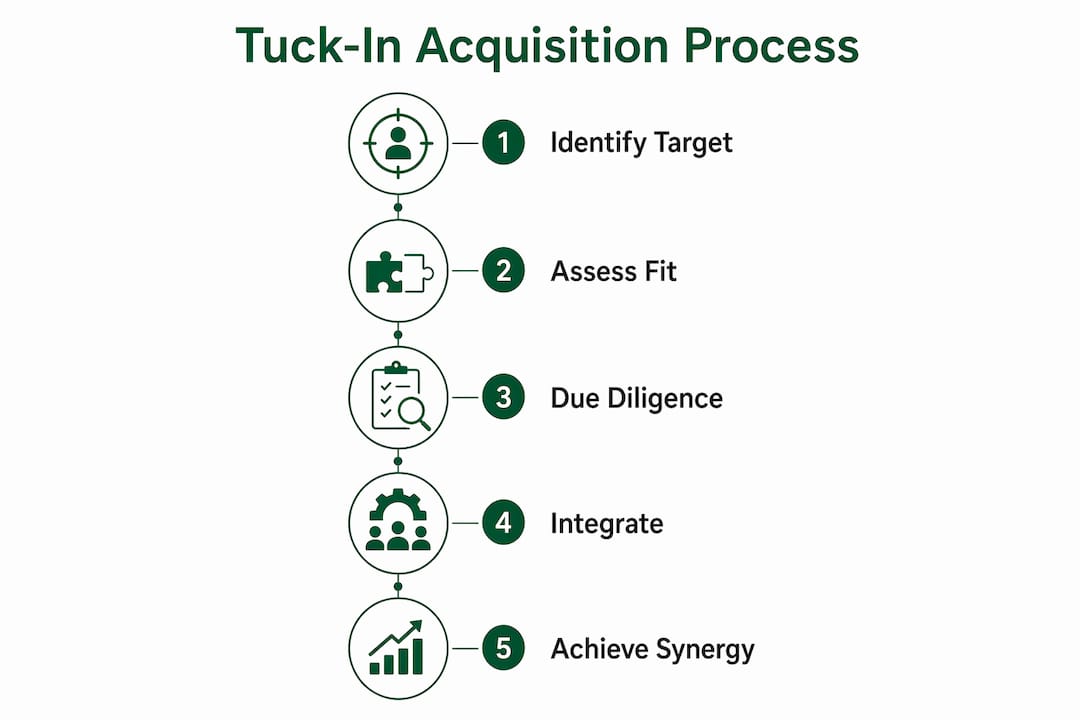

The process follows a clear sequence. The acquirer identifies a target that fills a specific gap, whether that is a customer segment, a technology, a geographic market, or a skilled team. Due diligence covers financials, operations, culture, and IT systems. A purchase agreement is signed, and integration begins. Integration planning must start from the first engagement, not after the deal closes, to protect the talent and assets that justified the acquisition in the first place.

The term “tuck-in” is informal industry shorthand. The recognized M&A category is a fully integrated acquisition, sometimes also called an absorptive acquisition. Both terms describe the same outcome: the target disappears into the acquirer’s structure completely.

What are the main benefits of tuck-in acquisitions?

Tuck-in deals deliver growth at a fraction of the cost and risk of large mergers. Tuck-in acquisitions carry lower financial risk than mega-mergers because the capital outlay is smaller and the integration scope is contained. That smaller scope also means faster time to value. A company can absorb a target and realize synergies within months rather than years.

The specific benefits break down as follows:

- Lower capital requirement. Smaller targets cost less to acquire. That frees capital for additional deals or organic investment.

- Faster capability gain. Buying a team with specialized skills or proprietary technology is faster than building those capabilities internally.

- Immediate customer base access. The acquired company’s customers transfer to the acquirer, expanding market reach without a sales cycle.

- Cost savings through consolidation. Redundant departments, such as finance, HR, and administration, merge into one, reducing overhead.

- Reduced integration complexity. A smaller target has fewer systems, fewer staff, and fewer stakeholder groups to align.

Tuck-in acquisitions provide new capabilities at lower cost than internal development, which is especially valuable in mature markets where organic growth is slow and expensive. A business that would take three years to build from scratch can be acquired and absorbed in three months.

Pro Tip: Before signing a letter of intent, map every operational function of the target against your own. Any overlap is a cost-saving opportunity. Any gap is a risk that needs a plan.

How does tuck-in acquisition differ from other acquisition strategies?

The clearest way to understand tuck-in acquisitions is to compare them against the two most similar deal types: bolt-on acquisitions and platform acquisitions.

| Acquisition type | Target identity post-deal | Integration depth | Typical deal size | Primary goal |

|---|---|---|---|---|

| Tuck-in | Fully absorbed, ceases to exist | Complete operational merger | Small | Add capability or customers to existing platform |

| Bolt-on | Partially retained or rebranded | Moderate, some autonomy kept | Small to mid-size | Expand product line or geography |

| Platform | Retained as operating entity | Minimal, target runs independently | Mid to large | Create a new business unit or market anchor |

A bolt-on acquisition keeps some of the target’s identity and operational independence. The acquirer adds the target to its portfolio but does not fully merge systems, staff, or branding. A platform acquisition is the opposite: the acquirer buys a sizeable business to serve as the foundation for future growth, then adds smaller deals around it.

A tuck-in sits at the most integrated end of the spectrum. The target’s brand, leadership structure, and operational independence all disappear. This depth of integration is what produces the cost savings and capability gains that make tuck-ins attractive. It also demands the most rigorous planning, because there is no fallback structure if integration fails.

Compared to a horizontal acquisition, where two companies of similar size in the same industry combine, a tuck-in involves a clear size asymmetry. The acquirer is significantly larger. That size difference makes full absorption practical and efficient.

What are the critical success factors and common pitfalls?

The most common failure point in tuck-in deals is not financial. Cultural and operational misalignment cause more deal failures than poor financial metrics. When the acquired team does not feel respected or informed, key people leave. When they leave, the capabilities that justified the acquisition leave with them.

The critical success factors are:

- Early stakeholder involvement. Operational leaders from both sides must engage before the deal closes. Early involvement of operational stakeholders correlates directly with integration success.

- Cultural due diligence. Assess management style, decision-making norms, and communication culture alongside financial statements.

- IT and systems audit. IT and systems compatibility is frequently overlooked but causes serious operational inefficiencies post-close. Audit CRM platforms, inventory systems, and data structures before signing.

- Transparent communication. Tell the acquired team what is changing, when, and why. Silence creates fear, and fear drives resignations.

- Rigorous due diligence regardless of deal size. The due diligence process for tuck-in acquisitions must be as thorough as for larger deals. Small deals are not simple deals.

Treating a small acquisition as a simple transaction is the fastest way to destroy the value you paid for. The talent, the customer relationships, and the institutional knowledge that made the target worth buying are all people-dependent. Lose the people, and you have bought an empty shell. Proactive communication and cultural integration are not soft skills. They are the primary value-protection tools in any tuck-in deal.

Pro Tip: Run a cultural assessment survey with the target’s leadership team during due diligence. Ask about decision-making speed, conflict resolution norms, and communication preferences. Mismatches here predict integration friction better than any financial model.

How do tuck-in acquisitions fit into roll-up strategies?

Tuck-in acquisitions become most powerful when used as part of a roll-up strategy. A roll-up starts with an anchor deal, where the acquirer buys a platform business of meaningful size. That platform then absorbs a series of smaller tuck-in targets over time, building scale deal by deal.

The advantages of this sequential approach over a single large acquisition are significant:

- Lower risk per transaction. Each deal is small enough that a failed integration does not threaten the whole business.

- Compounding synergies. Each tuck-in adds customers, capabilities, or cost savings that make the next deal more attractive.

- Faster valuation growth. A series of smaller deals can build enterprise value faster than waiting for one large opportunity.

- Repeatable process. After the first tuck-in, the acquirer has a tested integration playbook. Each subsequent deal runs faster and cheaper.

- Market consolidation. In fragmented industries, a roll-up strategy can establish market leadership within a few years.

A roll-up strategy with an anchor deal supported by sequential tuck-in acquisitions reliably builds scale. One documented case built a business worth £400 million through six acquisitions completed in 18 months. That pace of value creation is not achievable through organic growth alone.

The table below shows how a roll-up typically progresses:

| Phase | Activity | Outcome |

|---|---|---|

| Year 1: Anchor deal | Acquire platform business | Establish operational base |

| Year 1–2: First tuck-ins | Absorb 2–3 small targets | Add customers and capabilities |

| Year 2–3: Scale phase | Absorb 3–5 additional targets | Consolidate market position |

| Year 3+: Exit or expand | Sell or continue acquiring | Realize valuation premium |

Future M&A success belongs to companies that efficiently integrate smaller deals rather than those chasing huge transformational mergers. The roll-up model proves this point repeatedly across industries from professional services to technology distribution.

Understanding market analysis before acquiring each tuck-in target is what separates disciplined roll-ups from unfocused deal-making. Every target must fit a defined strategic gap, not just an available price.

Key Takeaways

A tuck-in acquisition strategy delivers the fastest, lowest-risk path to capability growth when integration planning starts at first contact and cultural alignment receives the same rigor as financial due diligence.

| Point | Details |

|---|---|

| Core definition | A tuck-in fully absorbs the target, which ceases to exist as an independent entity. |

| Primary advantage | Lower capital and risk than large mergers, with faster access to new capabilities and customers. |

| Biggest failure risk | Cultural and operational misalignment causes more deal failures than poor financials. |

| Integration timing | Planning must begin at first contact, not after the deal closes. |

| Roll-up potential | Sequential tuck-in deals around an anchor platform can build significant enterprise value rapidly. |

Why integration discipline separates tuck-in winners from losers

Most business leaders I work with underestimate one thing: the gap between signing a deal and realizing its value. That gap is where tuck-in acquisitions either succeed or quietly fail. The financial model looks clean. The synergy projections are compelling. Then the acquired team starts leaving, the IT systems do not connect, and the customers who came with the deal start drifting.

The leaders who get this right treat integration as a parallel workstream, not a follow-up task. They assign an integration lead before the deal closes. They communicate with the acquired team before the ink is dry. They audit IT systems during due diligence, not after. These are not complicated steps. They are disciplined ones.

The other thing I have seen consistently: smaller deals demand the same respect as large ones. The temptation to treat a tuck-in as a minor transaction leads directly to the cultural clashes and talent losses that erode deal value. Successful tuck-ins avoid treating small acquisitions as simple, and that discipline is what separates the acquirers who build lasting value from those who buy and then wonder what went wrong.

Tuck-ins are a repeatable growth lever when you treat them that way. Build a process, refine it with each deal, and the compounding effect on your business is real. Understanding deal negotiation timing is part of that process. So is knowing when to walk away from a target that looks right on paper but feels wrong in the room.

— Sierra

How Compassbusinessacquisitions supports your acquisition goals

Executing a tuck-in acquisition requires more than a good target list. It requires accurate valuations, market insight, and a network that surfaces the right opportunities before they reach the open market.

Compassbusinessacquisitions works with buyers pursuing targeted acquisitions and sellers ready to position their business for the right acquirer. The team provides professional valuations, targeted marketing, and direct guidance through every stage of the deal process. Whether you are building a roll-up strategy or evaluating your first tuck-in target, expert support reduces risk and improves outcomes. Explore businesses for sale and connect with advisors who understand what strategic fit actually means in practice.

FAQ

What is the difference between a tuck-in and a bolt-on acquisition?

A tuck-in fully absorbs the target, which ceases to exist independently. A bolt-on keeps some of the target’s operational identity and runs with partial autonomy inside the acquirer’s portfolio.

How long does a tuck-in acquisition integration typically take?

Integration timelines vary by deal complexity, but tuck-ins generally complete faster than large mergers because the target is smaller and the scope is contained. Planning from first contact shortens the timeline further.

What industries use tuck-in acquisitions most often?

Tuck-in acquisitions are common in mature, fragmented industries where organic growth is costly and slow, including professional services, technology, healthcare services, and distribution.

Why do tuck-in acquisitions fail?

Cultural and operational misalignment cause most failures. Acquirers who skip cultural due diligence or delay communication with the acquired team lose key personnel and the value they carried.

How do I identify a good tuck-in acquisition target?

A strong target fills a defined gap in your operations, whether that is a customer segment, technology, or geography. Conducting thorough market analysis before acquiring confirms whether the target’s position is defensible and worth the integration effort.