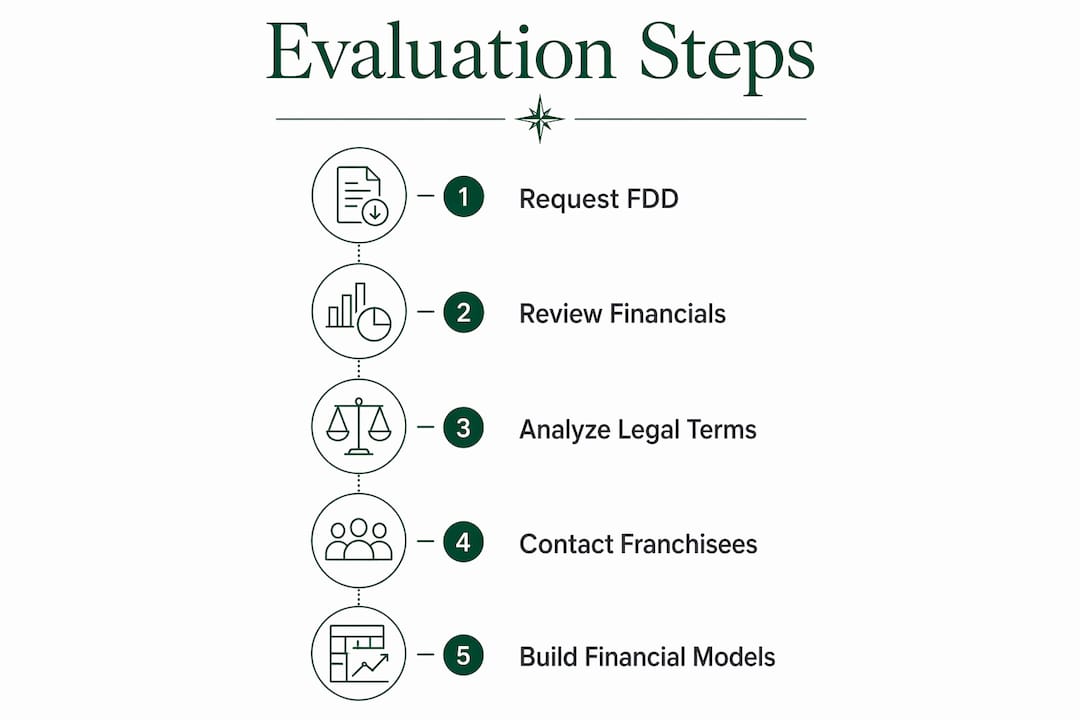

How to Evaluate Franchise Acquisition Opportunities

How to Evaluate Franchise Acquisition Opportunities

Evaluating franchise acquisition opportunities is a structured process of analyzing a franchise’s financial health, legal framework, operational support, and market potential to determine its viability. The industry term for this process is franchise due diligence, and skipping any part of it is the most common reason buyers overpay or fail. The Franchise Disclosure Document (FDD), mandated by the FTC, is the starting point for every serious investor. Healthy franchise benchmarks in 2026 include an 18–35% cash-on-cash return in Year 2, an EBITDA margin of 12–22%, and total fees under 10% of revenue. These numbers give you a clear baseline before you commit a dollar.

How to evaluate franchise acquisition opportunities: the FDD and key documents

The Franchise Disclosure Document is the legal foundation of every franchise purchase evaluation. The FTC requires franchisors to deliver it at least 14 days before signing any agreement. That waiting period exists for a reason. Use every day of it.

Six items inside the FDD deserve the most attention:

- Item 7: Total estimated initial investment, including fees, equipment, and working capital.

- Item 12: Territory rights, exclusivity scope, and conditions under which the franchisor can encroach.

- Item 19: Financial performance representations, the only place franchisors can legally share unit-level revenue data.

- Item 20: Outlet information showing openings, closures, terminations, and transfers over the past three years.

- Item 21: Audited financial statements revealing the franchisor’s own financial health.

- Item 3: Litigation history, including lawsuits filed by or against the franchisor.

Audited financial statements in Item 21 tell you whether the franchisor can actually support its network. A franchisor with thin margins or declining revenue cannot fund training, marketing, or field support reliably.

Pro Tip: Request the FDD as early as possible, even before you are ready to sign. Reading it without deadline pressure lets you spot red flags without the emotional pull of a closing timeline.

Contacting franchisees listed in Item 20 is non-negotiable. Former franchisees give the most candid feedback because they have no incentive to protect the brand. Ask them why they left. Their answers will tell you more than any sales presentation.

How to build and interpret franchise financial models

Financial modeling is where franchise investment analysis becomes concrete. The goal is to build three scenarios: conservative, base, and optimistic. Modeling multiple scenarios and stress-testing assumptions is the standard practice for serious franchise buyers.

Follow this sequence to build a reliable model:

- Set revenue projections. Use Item 19 data as your baseline. If Item 19 is absent, use industry benchmarks from trade associations or comparable franchise systems.

- Calculate total investment. Pull Item 7 figures and add a contingency buffer of 10–20% above the franchisor’s estimate.

- Model operating expenses. Include royalties, marketing fund contributions, rent, labor, cost of goods sold, and insurance.

- Calculate key metrics. Focus on cash-on-cash return, EBITDA margin, internal rate of return (IRR), and payback period.

- Stress-test the model. Run a scenario where Year 1 revenue comes in 20–30% below your base case. If the business still survives, the investment has real resilience.

Base-case franchise investments average 22% IRR over five years, with break-even typically between 18 and 42 months. That range is wide, which is exactly why your model needs to reflect your specific location, labor market, and lease terms.

| Metric | Healthy Benchmark | Red Flag |

|---|---|---|

| Cash-on-cash return (Year 2) | 18–35% | Below 10% |

| EBITDA margin | 12–22% | Below 8% |

| Total fees as % of revenue | Under 10% | Above 15% |

| Annual franchise mortality rate | Below 8% | Above 10% |

| Break-even period | 18–42 months | Over 48 months |

Working capital is where most buyers make their biggest mistake. Recommended working capital covers 3–6 months of operating expenses, and that figure often exceeds franchisor estimates by $30,000 to $100,000. Budget for the real number, not the optimistic one.

Pro Tip: If an SBA 7(a) loan is part of your financing plan, check the franchisor’s SBA default rate. An SBA default rate under 5% is a strong predictor of franchisee success and signals that the system produces viable businesses.

What legal terms and territorial rights reveal about risk

Legal review is not optional. A franchise attorney who specializes in FDD analysis pays for itself many times over. The contract clauses that look minor in a sales meeting can cost you control of your business years later.

Critical legal red flags include:

- Unilateral territory relocation: The franchisor can move your protected area without your consent.

- Mandatory remodels without cost caps: You absorb unlimited renovation costs on the franchisor’s schedule.

- Personal guarantees: Your personal assets are at risk if the business fails.

- Overly restrictive non-competes: Post-term clauses that prevent you from working in your own industry for years.

- Mandatory arbitration in the franchisor’s home state: Forces you to litigate far from home, at significant cost.

Careful scrutiny of contract clauses on termination rights, territory exclusivity, and remodeling obligations can prevent costly future surprises and preserve franchisee control. A single overlooked clause can eliminate your ability to sell, renew, or exit on your own terms.

Territory analysis under Item 12 goes beyond just reading the geographic description. Verify the demographic data inside your protected area. A territory that looks large on a map may have insufficient population density, household income, or consumer demand to support your revenue projections.

Franchise mortality rate above 8–10% annually signals major systemic failures. Calculate it yourself from Item 20 data rather than accepting the franchisor’s summary. Add terminations and non-renewals over three years, divide by the average number of outlets, and you have the real attrition rate. A high number is an early disqualification criterion, not a negotiating point.

How to conduct franchisee validation and market analysis

Franchisee validation is the most underused tool in franchise opportunity assessment. Most buyers call two or three franchisees from a list the franchisor provides. That is not enough. Call at least ten, and make sure several are from the Item 20 exit list.

Use this sequence for productive validation interviews:

- Ask about unit economics first. Request actual revenue ranges, not just whether they are “happy.” Franchisees who share numbers are the most credible.

- Probe support quality. Ask how quickly the franchisor responds to operational problems and whether training prepared them for real conditions.

- Ask about the hardest part. The answer reveals operational realities the FDD never mentions.

- Contact former franchisees directly. Former franchisees provide the most honest picture of why people leave the system.

- Compare their experience to Item 19 data. If top performers are far above the median, the system may have structural inequality built in.

Market analysis runs parallel to franchisee validation. Use demographic data from the U.S. Census Bureau to verify population density, median household income, and age distribution within your territory. Layer in competitive mapping to identify how many direct and indirect competitors already operate nearby. A market analysis approach that combines demographic data with competitive density gives you a realistic revenue ceiling before you sign anything.

Operational fit matters as much as financial fit. Ask yourself whether the daily work of running this franchise aligns with your skills and schedule. A franchise with strong unit economics but a 70-hour work week is not a good investment if you cannot sustain that pace.

Pro Tip: Spousal and partner alignment is critical for franchise success. Financial and operational buy-in from everyone affected by the decision must happen before you sign, not after.

Key Takeaways

Franchise due diligence succeeds when you treat it as an early-disqualification process, not a confirmation checklist, using FDD data, financial modeling, legal review, and franchisee validation together.

| Point | Details |

|---|---|

| FDD is the foundation | Review Items 7, 12, 19, 20, and 21 before any other step in your evaluation. |

| Model three financial scenarios | Build conservative, base, and optimistic projections and stress-test each against a 20–30% revenue shortfall. |

| Legal review is non-negotiable | A franchise attorney must review termination rights, territory clauses, and non-compete terms before you sign. |

| Mortality rate reveals system health | Calculate attrition from Item 20 yourself; a rate above 8–10% annually is a disqualification signal. |

| Validation requires former franchisees | Contact at least ten franchisees, including those who left, to get an accurate picture of real unit economics. |

What I’ve learned about buying franchises the right way

The best franchise buyers treat acquisitions like private equity investments, rigorously modeling returns and managing risk at every step. After working through dozens of franchise evaluations, I can tell you that the buyers who struggle most are the ones who fall in love with a brand before they finish reading the FDD.

The most common mistake I see is underestimating working capital. Buyers accept the franchisor’s estimate as gospel, then run short of cash in months four through eight when revenue is still ramping. The real number is almost always higher. Budget for 3–6 months of full operating expenses from your own calculations, not the disclosure document’s footnotes.

The second mistake is treating due diligence as a confirmation exercise. Due diligence works best as an early-disqualification tool. You are not trying to find reasons to buy. You are trying to find reasons to walk away before the reasons find you. The moment you catch yourself rationalizing a red flag, stop and call your franchise attorney.

Patience is the most underrated skill in franchise acquisition. The right opportunity will survive a thorough 60-day review. If a franchisor pressures you to sign before you finish your analysis, that pressure itself is a red flag worth noting. Good systems welcome scrutiny. Weak ones discourage it.

— Sierra

Franchise acquisition support from Compassbusinessacquisitions

Serious investors know that the right advisory team changes the outcome of a franchise acquisition. Compassbusinessacquisitions brings professional valuation, market analysis, and negotiation support to every transaction, connecting buyers with opportunities that match their financial goals and operational capacity.

Whether you are evaluating your first franchise or adding to an existing portfolio, Compassbusinessacquisitions provides the due diligence guidance and market insight needed to make a confident decision. The team’s network spans multiple industries and markets, giving buyers access to vetted opportunities with verifiable financials and clear growth potential. Visit Compassbusinessacquisitions to connect with an advisor and start your evaluation with a clear framework and professional support behind you.

FAQ

What is the Franchise Disclosure Document?

The Franchise Disclosure Document (FDD) is a legally required disclosure the FTC mandates franchisors provide at least 14 days before any agreement is signed. It contains 23 items covering fees, financials, litigation history, and franchisee outlet data.

What financial return should I expect from a franchise?

Healthy franchise investments target an 18–35% cash-on-cash return in Year 2, an EBITDA margin of 12–22%, and a break-even period between 18 and 42 months, based on 2026 industry benchmarks.

How do I calculate franchise system health from Item 20?

Add terminations and non-renewals from the past three years, then divide by the average number of active outlets. A resulting annual mortality rate above 8–10% signals systemic problems and warrants disqualification.

Why should I contact former franchisees?

Former franchisees have no incentive to protect the brand and provide the most candid feedback on unit economics, support quality, and the real reasons people exit the system.

How much working capital do I actually need?

Working capital needs typically cover 3–6 months of total operating expenses, and that figure often exceeds franchisor estimates by $30,000 to $100,000. Calculate the number yourself using your actual projected costs.