Business Sale Closing Process: A Small Business Owner's Guide

Business Sale Closing Process: A Small Business Owner’s Guide

The business sale closing process is the formal finalization of a business transaction, where ownership legally transfers from seller to buyer through signed contracts, funds exchange, and completed government filings. Most small business owners treat closing as a single event, but it is actually a structured sequence of legal, financial, and operational steps. Missing any one of them can delay or kill a deal. Understanding what is a business sale closing process gives you the clarity to move through it with confidence and protect the value you have built.

What key documents are involved in the business sale closing process?

The closing requires signing a Purchase Agreement, Bill of Sale, non-compete agreements, assignment of leases, and escrow instructions to formalize the sale. Each document serves a distinct legal purpose, and none of them are optional.

Here is what each core document does:

- Purchase Agreement: This is the primary contract. It covers the sale price, payment terms, warranties, indemnifications, and price adjustment mechanisms. Purchase Agreements often run 40–80 pages. Every seller should read it in full with an attorney before signing.

- Bill of Sale: This document transfers specific assets from seller to buyer. It lists equipment, inventory, intellectual property, and goodwill. Without it, asset ownership remains legally ambiguous.

- Non-compete and confidentiality agreements: Buyers require these to protect the business they are acquiring. A non-compete typically restricts the seller from opening a competing business within a defined geography and time period.

- Promissory note and security agreement: These apply when the seller provides financing. The promissory note defines repayment terms. The security agreement gives the seller a lien on business assets if the buyer defaults.

- Assignment of leases and contracts: Existing leases, supplier contracts, and customer agreements must transfer to the buyer. Landlords and counterparties often need to approve these assignments in writing.

- Closing statement and funds flow memo: This document maps exactly where every dollar goes at closing, covering payoffs, escrow funding, taxes, and adjustments. Errors in the funds flow memo are among the most common causes of last-minute deal failures.

- IRS and government filings: Depending on the deal structure, you may need to file IRS Form 8594 (Asset Acquisition Statement) and notify state agencies of the ownership change.

Pro Tip: Request a complete closing checklist from your attorney at least 30 days before the scheduled closing date. Tracking every document in a shared folder prevents last-minute scrambles.

What are the typical steps and timeline from signing to closing?

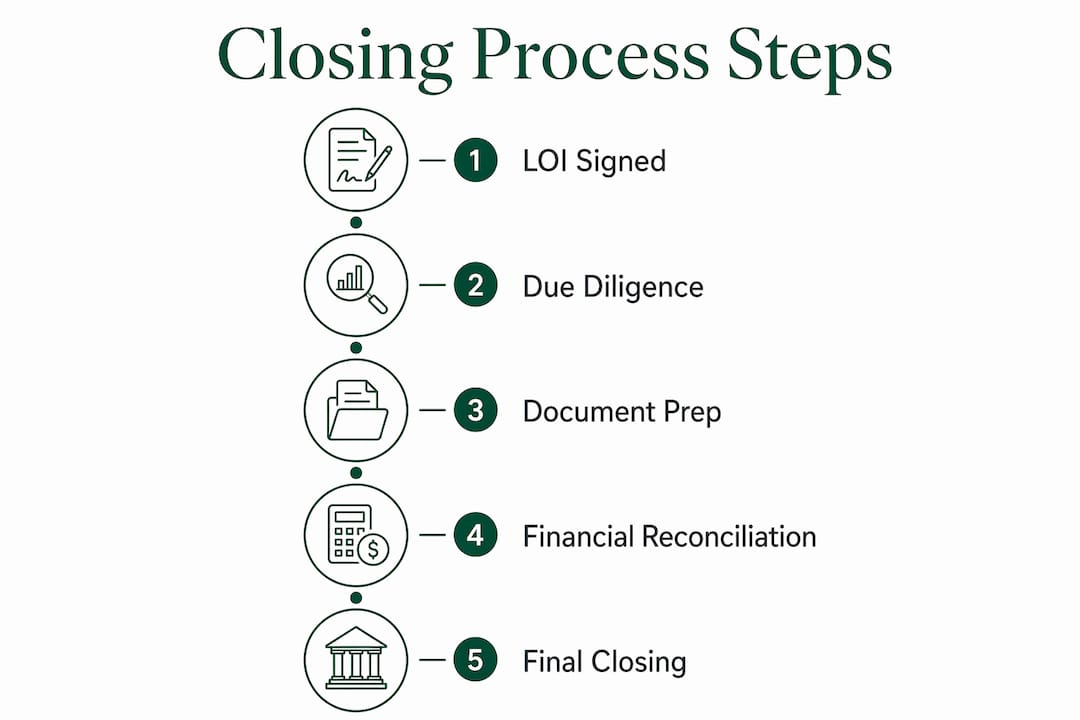

Selling a business usually takes six to nine months from Letter of Intent to closing, plus additional months or years for pre-market preparation. Owners who underestimate this timeline often accept lower prices or rushed terms. The stages of the business sale process follow a predictable sequence.

-

Letter of Intent (LOI) signing. The LOI marks the transition from negotiation to due diligence and outlines basic deal terms: price, payment structure, and transition commitments. Once signed, the buyer’s negotiating leverage increases. Sellers should negotiate LOI terms carefully before signing.

-

Due diligence. Buyers review financials, tax returns, leases, contracts, payroll records, and vendor relationships. This stage typically runs four to eight weeks. Gaps or inconsistencies discovered here give buyers grounds to renegotiate or walk away.

-

Purchase Agreement drafting and negotiation. Attorneys for both sides draft and negotiate the Purchase Agreement based on due diligence findings. This phase often takes two to four weeks. Price adjustments, indemnification caps, and warranty terms are the most contested points.

-

Financing approvals and contingencies. If the buyer uses an SBA loan or bank financing, lender approval must be secured before closing. This step can add four to twelve weeks to the timeline. Sellers should confirm financing status early and often.

-

Closing document preparation. Attorneys prepare the full closing package: all agreements, assignments, resolutions, and the funds flow memo. Both parties review and approve the package before closing day.

-

Closing day. Most small business sales are “sign and close” transactions, where ownership transfer and funds exchange occur on the same day. All parties sign documents, funds wire to the appropriate accounts, and the business legally changes hands.

-

Post-closing transition. Working capital adjustments settle within 30–90 days. Post-closing activities include transferring licenses, notifying the IRS and state agencies, updating insurance policies, and communicating changes to employees and customers.

What financial reconciliations happen at closing?

Purchase price adjustments are one of the most misunderstood parts of the business sale process. The final amount you receive at closing often differs from the agreed headline price. Here is how the key adjustments work.

| Adjustment Type | What It Covers | Who It Affects |

|---|---|---|

| Working capital true-up | Difference between target and actual closing-day working capital | Buyer and seller |

| Escrow holdback | Funds held post-closing to cover indemnification claims | Seller receives after release period |

| Prorated expenses | Rent, utilities, and insurance split by closing date | Both parties |

| Seller financing payoff | Outstanding loans paid from proceeds at closing | Seller and lender |

| Tax withholdings | State and federal taxes due on sale proceeds | Seller |

Working capital adjustments post-closing are common and disputes over them are often resolved by independent accounting firms. The target working capital figure is set in the Purchase Agreement. If actual closing-day working capital falls short, the seller pays the difference. If it exceeds the target, the seller receives a bonus payment.

The funds flow memo drives all of this. Sellers and buyers review it carefully before closing to prevent mistakes. A single error in this document can delay wire transfers and push closing to the next business day, which creates cascading problems for both parties.

Pro Tip: Ask your accountant to prepare a projected closing-day balance sheet at least two weeks before closing. Comparing it to the target working capital figure reveals any gaps while you still have time to address them.

How to prepare for a smooth closing and avoid common pitfalls

Preparation is the single biggest factor in whether a closing goes smoothly or falls apart. Thorough pre-sale preparation, including auditing the business from a buyer’s perspective years in advance, markedly improves closing success and final sale price. Here is a practical business closing checklist to guide your preparation.

- Organize all financial records. Gather three years of tax returns, profit and loss statements, balance sheets, and bank statements. Buyers and lenders will request all of them.

- Audit your contracts and leases. Identify which agreements require landlord or counterparty consent to assign. Start those conversations early. Delays in lease assignments are a top reason closings get pushed back.

- Resolve outstanding liabilities. Pay off or document any liens, unpaid taxes, or pending lawsuits before closing. Undisclosed liabilities discovered at closing give buyers grounds to reduce the price or walk away.

- Coordinate your advisory team. Your attorney, accountant, and business broker need to work together. Miscommunication between advisors is a common source of document errors and timeline slippage. Compassbusinessacquisitions coordinates this process for sellers to keep all parties aligned.

- Prepare your employees and customers. A clear communication plan maintains goodwill and operational continuity. Decide in advance what you will say, when you will say it, and who will deliver the message.

- Review emotional pitfalls in selling. Sellers often underestimate how emotionally demanding the closing period is. Fatigue and stress lead to rushed decisions on final terms.

- Understand your exit options. Your business exit strategy shapes which closing structure makes the most sense for your situation.

Employment agreements, non-compete clauses, and transition service arrangements are signed at closing or shortly after. These protect the buyer and give the business continuity. Sellers who resist these agreements often lose deals or face price reductions.

Key Takeaways

The business sale closing process succeeds when sellers prepare documents early, coordinate advisors, and understand every financial adjustment before closing day arrives.

| Point | Details |

|---|---|

| Closing is a structured sequence | The process runs from LOI through due diligence, document drafting, and closing day. |

| Documents drive the deal | The Purchase Agreement, Bill of Sale, and funds flow memo are non-negotiable closing requirements. |

| Financial adjustments are common | Working capital true-ups and escrow holdbacks often change the final amount you receive. |

| Timeline is longer than expected | Most sales take six to nine months from LOI to closing, not counting pre-market preparation. |

| Early preparation prevents failure | Organizing records and resolving liabilities before closing day eliminates the most common deal-killers. |

What I have learned about closing a business sale

The part of the closing process that surprises sellers most is not the paperwork. It is the pace. You spend months building toward a closing date, and then everything accelerates in the final two weeks. Documents arrive for review, attorneys request revisions, lenders ask for updated financials, and the funds flow memo goes through three drafts. Sellers who have not organized their records in advance find themselves scrambling to produce documents they should have had ready months earlier.

The second thing that catches sellers off guard is working capital. Most sellers focus on the headline price and assume that is what they will receive. Then the closing-day balance sheet comes in below the target, and the adjustment reduces their proceeds by tens of thousands of dollars. This is not a trick. It is a standard mechanism. But sellers who understand it in advance negotiate the target figure more carefully and monitor their working capital in the months before closing.

My honest view is that closing is not a single event. It is the final chapter of a process that started the day you decided to sell. The sellers who close successfully are the ones who treated preparation as a continuous activity, not a last-minute task. They audited their own business, resolved liabilities, and built a team of advisors who communicated well. The closing itself was almost anticlimactic for them. That is exactly what you want.

— Sierra

Compassbusinessacquisitions can guide you through every closing stage

Closing a business sale involves more moving parts than most sellers anticipate. Compassbusinessacquisitions works with sellers to coordinate attorneys, accountants, and buyers so that every document, adjustment, and deadline stays on track.

Whether you are preparing your first sale or navigating a complex transaction, Compassbusinessacquisitions provides professional valuations, targeted marketing, and hands-on support from LOI through post-closing transition. Their network and market knowledge help sellers maximize value and close with confidence. Connect with the team at Compassbusinessacquisitions to get personalized guidance on your sale and learn what your business is worth today.

FAQ

What is a business sale closing process?

The business sale closing process is the formal sequence of steps where a seller and buyer sign legal documents, exchange funds, and transfer ownership of a business. It includes executing the Purchase Agreement, Bill of Sale, and all supporting agreements on or before closing day.

How long does the business sale closing process take?

Most small business sales take six to nine months from the Letter of Intent to closing. Pre-market preparation can add additional months or years depending on how ready the business is for sale.

What documents are required to close a business sale?

The core documents include the Purchase Agreement, Bill of Sale, non-compete agreements, assignment of leases, promissory notes if seller financing applies, and the funds flow memo. IRS Form 8594 is also required for asset sales.

What are closing costs for a business sale?

Closing costs such as attorney and closing agent fees are often split 50/50 between buyer and seller, typically ranging between $1,000 and $2,000 per party, though deal complexity can push costs higher.

What happens after a business sale closes?

Post-closing activities include transferring licenses and permits, notifying the IRS and state agencies, updating insurance policies, and communicating ownership changes to employees and customers. Working capital adjustments typically settle within 30–90 days of closing.